What are the new income tax rates under the TRAIN or Tax Reform for Acceleration and Inclusion law? How will TRAIN affect the preparation of Income Tax Returns (ITR) of individuals and corporations? How is the TRAIN tax system different from the previous tax system of the Philippines?

In this article, we focus on answering these questions. You can also download below the new TRAIN Income Tax Tables adopted by the Bureau of Internal Revenue (BIR), with sample computations showing how income taxes can be calculated under the new tax regime.

For context, the Philippines’ latest tax reform bill, known as TRAIN or Tax Reform for Acceleration and Inclusion, was signed into law on December 19, 2017. Its implementation began on January 1, 2018.

First off, take note that in the new TRAIN tax law, there are two (2) sets of income tax tables to be implemented:

(1) Income Tax Tables that will be used from year 2023 onwards; and

(2) Income Tax Tables used during the initial or transitory period from 2018 to 2022.

NOTE: We also compiled various articles related to the TRAIN law on this page: TRAIN Tax Law, Sample Computations, and BIR Implementing Guidelines. Click the link to access relevant information, such as the following useful articles on Philippine taxation.

- Are Online Sellers & YouTubers Required to Pay Taxes to BIR?

- Top 10 Highest Paid YouTubers in the Philippines

- 10 TRAIN Tax Reform Items that You Probably Didn’t Know

- BIR Sample Computations: How to Compute Taxes under TRAIN

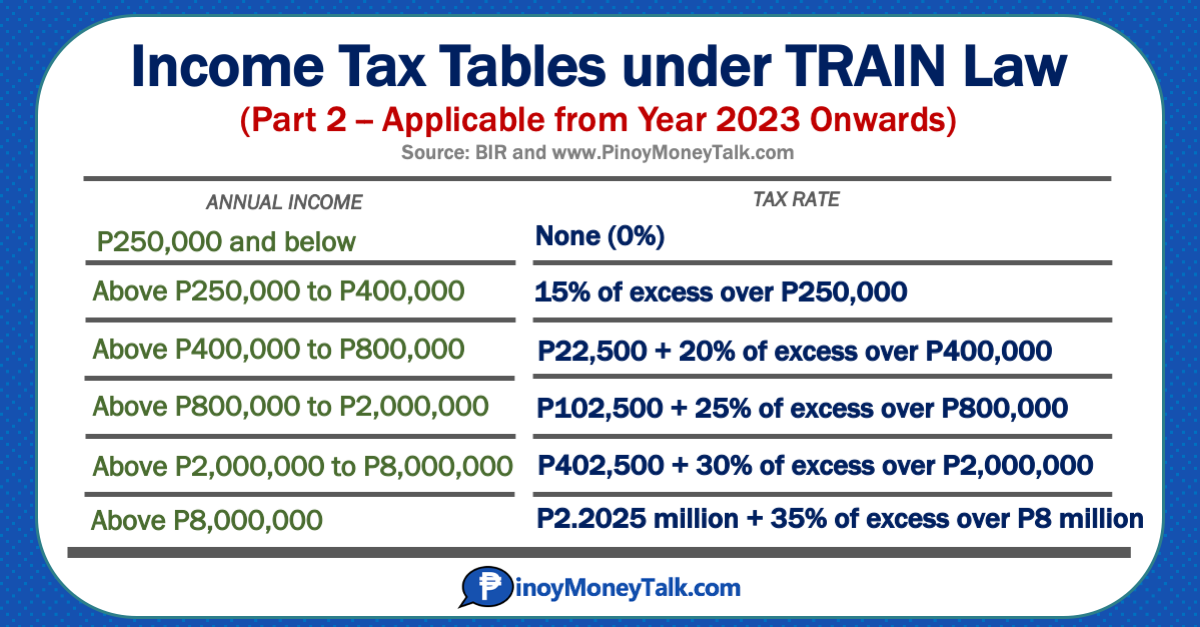

BIR Income Tax Rates under TRAIN (2023 onwards)

What are the important points related to the new income tax rates from 2023 and in succeeding years? From year 2023 onwards, the income tax rates under TRAIN will further be lowered, summarized as follows:

(i) Those earning annual salary of P250,000 or below will continue to be exempted from paying income tax; (ii) Those earning between P250,000 and P400,000 per year will be charged a lower income tax rate of 15% on the excess over P250,000; (iii) Those with annual salaries from P400,000 to P800,000 will have withholding taxes of P22,500 plus 20% of the excess over P400,000; (iv) Salaried employees with annual incomes between P800,000 and P2 million will be charged a fixed amount of P102,500 plus 25% on the excess over P800,000; (v) Those receiving salaries between P2 million and P8 million per year will be charged P402,500 plus 30% of the excess over P2 million; and (vi) Finally, the highest income segment of employees with annual salaries of at least P8 million will pay P2.2025 million plus 35% of the excess over P8 million.

The new income tax rates from year 2023 onwards, as per the TRAIN law, are as follows.

| Taxable Income per Year | Income Tax Rate (Year 2023 onwards) |

|---|---|

| P250,000 and below | 0% |

| Above P250,000 to P400,000 | 15% of the excess over P250,000 |

| Above P400,000 to P800,000 | P22,500 + 20% of the excess over P400,000 |

| Above P800,000 to P2,000,000 | P102,500 + 25% of the excess over P800,000 |

| Above P2,000,000 to P8,000,000 | P402,500 + 30% of the excess over P2,000,000 |

| Above P8,000,000 | P2,202,500 + 35% of the excess over P5,000,000 |

| Source: | BIR and PinoyMoneyTalk.com |

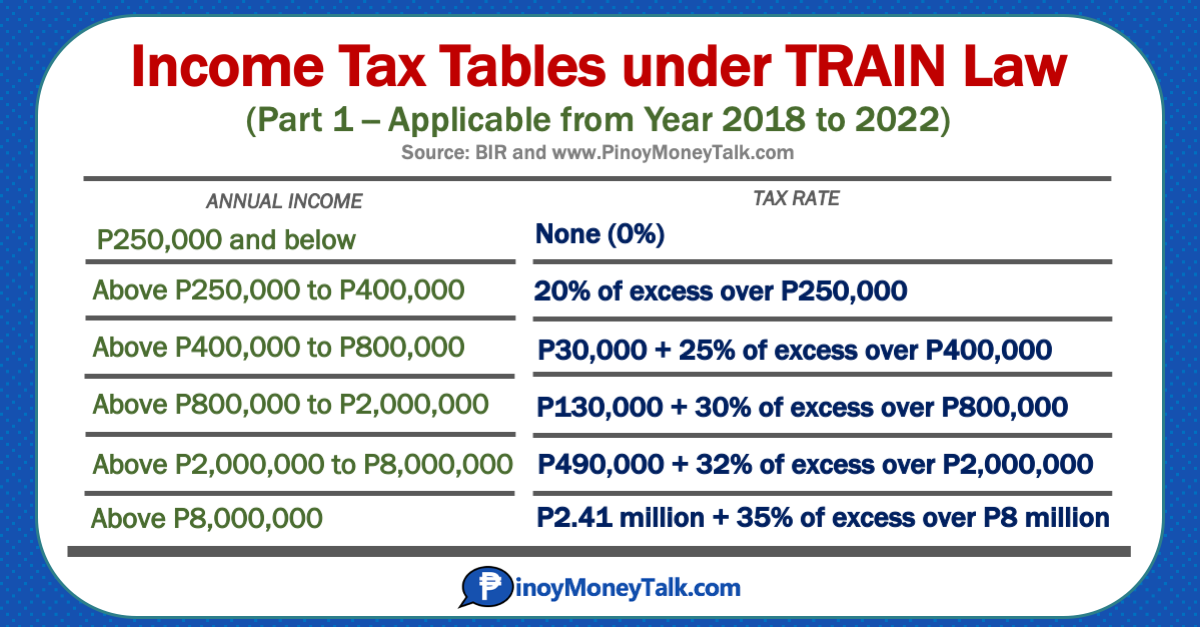

Income Tax Rates under TRAIN (from 2018-2022)

The first part of the approved TRAIN tax reform law, implemented from 2018 until 2022, adopted major changes from the then existing Philippine taxation system, as follows:

(i) Those earning an annual salary of P250,000 or below will no longer pay income tax (zero income tax); (ii) Those earning between P250,000 and P400,000 per year will be charged an income tax rate of 20% on the excess over P250,000; (iii) Those earning annual incomes between P400,000 and P800,000 will pay a fixed amount of P30,000 plus 25% of the excess over P400,000; (iv) Those with yearly salaries between P800,000 and P2 million will be charged a fixed amount of P130,000 plus 30% on the excess over P800,000; (v) High-income earners receiving salaries between P2 million and P8 million annually will pay a fixed amount of P490,000 plus 32% of the excess over P2 million; (vi) Finally, the highest income tier receiving salaries of at least P8 million per year will have withholding taxes of P2.41 million plus 35% of the excess over P8 million.

The updated TRAIN tax rates are as follows. Again, these rates only governed income taxes applicable during the period 2018 until 2022.

From year 2023 onwards, make sure you use the revised income tax rates in the earlier section. Again, as mentioned earlier, beginning 2023, the new income tax rates are actually lower than those implemented from 2018 to 2022.

| Taxable Income per Year | Income Tax Rate (Year 2018-2022) |

|---|---|

| P250,000 and below | 0% |

| Above P250,000 to P400,000 | 20% of the excess over P250,000 |

| Above P400,000 to P800,000 | P30,000 + 25% of the excess over P400,000 |

| Above P800,000 to P2,000,000 | P130,000 + 30% of the excess over P800,000 |

| Above P2,000,000 to P8,000,000 | P490,000 + 32% of the excess over P2,000,000 |

| Above P8,000,000 | P2,410,000 + 35% of the excess over P8,000,000 |

| Source: | BIR and PinoyMoneyTalk.com |

New TRAIN Income Tax Rates vs. Old Income Tax Rates

What changed in the new TRAIN tax law versus the old income tax law?

Prior to the approval and implementation of the TRAIN law in 2018, the following tax tables were in use until the end of 2017. The income tax rates before TRAIN, which are relatively higher than the post-TRAIN tax rates, are shown below.

| Income per Year | Income Tax Rate (Before TRAIN) |

|---|---|

| P10,000 and below | 5% |

| Above P10,000 to P30,000 | P500 + 10% of the excess over P10,000 |

| Above P30,000 to P70,000 | P2,500 + 15% of the excess over P30,000 |

| Above P70,000 to P140,000 | P8,500 + 20% of the excess over P70,000 |

| Above P140,000 to P250,000 | P22,500 + 25% of the excess over P140,000 |

| Above P250,000 to P500,000 | P50,000 + 30% of the excess over P250,000 |

| Above P500,000 | P125,000 + 32% of the excess over P500,000 |

| Source: | BIR and PinoyMoneyTalk.com |

Here are major items that changed when we compared the old (pre-TRAIN) tax tables versus the new TRAIN income tax tables.

1) income brackets were streamlined and reduced to just six (6) from seven (7) brackets; 2) taxable income threshold per bracket has been adjusted upwards; 3) tax rate charged on each taxable income bracket was revised, mostly lowered; 4) annual gross income eligible for tax exemption has been adjusted upwards from, previously, the amount of minimum wage to P250,000 in the new tax tables; and 5) personal exemption (P50,000) and additional exemptions (maximum of P100,000, if taxpayer has four dependents) were removed.

Under the TRAIN law, salaried individuals earning annual gross compensation of P250,000 or below are now exempted from paying income taxes. This is a drastic change from the past, wherein only minimum wage earners have been exempted.

What happened to personal and additional exemptions in the new TRAIN Income Tax law? The new TRAIN tax law removed these monetary exemptions previously enjoyed under the old Philippine tax system.

This means the Personal Exemption, amounting to P50,000, and additional exemption of P25,000 per qualified dependent (maximum of P100,000 additional exemptions for a taxpayer with four dependents) are now gone under the TRAIN law.

Sample Income Tax Computations under TRAIN (2018 to 2022)

How to compute income taxes under the new TRAIN law?

The formula to follow is simple. The formula that can be used to compute income tax due, under TRAIN’s graduated income tax rates, is:

INCOME TAX DUE = a + (b x c) where: a = Basic Amount of Annual Income; b = Additional Rate; and c = Of the Excess over the threshold amount

Let’s see some examples.

Sample Problem #1. How much is the income tax due of Employee Z whose taxable income was P300,000 for the year 2022?

The income tax payable can be computed by determining the appropriate row in the “Range of Taxable Income” which you can find below and calculating the Tax Due using the formula a + (b x c).

| Range of Taxable Income | TAX DUE = a + (b x c) | |||

|---|---|---|---|---|

| Over | Not Over | Basic Amount (a) | Additional Rate (b) | Of Excess Rate (c) |

| - | P250,000 | - | - | |

| P250,000 | P400,000 | - | 20% | P250,000 |

| P400,000 | P800,000 | P30,000 | 25% | P400,000 |

| P800,000 | P2,000,000 | P130,000 | 30% | P800,000 |

| P2,000,000 | P8,000,000 | P490,000 | 32% | P2,000,000 |

| P8,000,000 | - | P2,410,000 | 35% | P8,000,000 |

To recap, here’s the graduated TRAIN tax tables that we’ll use (a summary of the table above). Take note that what we’re using are the tax tables from 2018-2022 since we’re still computing the tax due of the employee for the year 2022.

To explain in detail, if the employee’s taxable income is P300,000, this will fall under the income bracket “Above P250,000 to P400,000”. The income tax due computation is as follows:

a = Basic Amount of Annual Income = Zero (0) b = Additional Rate = 20% c = Of the Excess over P250,000 = P50,000 INCOME TAX DUE = a + (b x c) INCOME TAX DUE = 0 + (20% * P50,000) = P10,000

Thus, Employee Z who earned taxable income of P300,000 in 2022 will pay income tax amounting to P10,000 under TRAIN.

With tax due of P10,000 on annual income of P300,000, the effective income tax rate charged to this taxpayer is only 3.33% — computed as P10,000 divided by P300,000 — definitely a much lower effective income tax rate vs. the previous tax system.

How about someone making P1 Million a year? What’s the income tax due? Let’s compute in the next example.

Sample Problem #2. Employee X works as an accountant in a company, with taxable income of P1,000,000 for the year 2022. How much is Employee X’s income tax payable? In addition, what is the effective income tax rate charged to Employee X?

Using the ITR tax tables above, we can see that the taxpayer falls under the tax bracket “Above P800,000 to P2,000,000”. Thus, the tax due is:

a = Basic Amount of Annual Income = P130,000 b = Additional Rate = 30% c = Of the Excess over P800,000 = P200,000 INCOME TAX DUE = a + (b x c) INCOME TAX DUE = P130,000 + (30% * P200,000) = P190,000

The accountant that earned taxable income of P1 Million in 2022 will record income tax of P190,000 in the ITR.

Also, the effective income tax rate charged to Employee X is 19% — computed as P190,000 divided by taxable income of P1 Million.

Sample Problems – Income Tax Computations under TRAIN (for 2023 onwards)

What about income tax computations for the year 2023 and onwards? The process is generally the same, but the ITR tax table to use will now be different. Here are examples.

Sample Problem #3. Employee Z is married with two dependents and earned taxable income of P300,000 in 2023. What will be Employee Z’s income tax due?

Take note that part 2 of TRAIN’s tax rates took effect beginning year 2023, so the new tax table to use is as follows.

Employee Z’s taxable income falls under the income bracket “Above P250,000 to P400,000”. The formula to follow is still the same as in sample problem #1, but the figures will be different.

| Range of Taxable Income | TAX DUE = a + (b x c) | |||

|---|---|---|---|---|

| Over | Not Over | Basic Amount (a) | Additional Rate (b) | Of Excess Rate (c) |

| – | P250,000 | – | – | |

| P250,000 | P400,000 | – | 15% | P250,000 |

| P400,000 | P800,000 | P22,500 | 20% | P400,000 |

| P800,000 | P2,000,000 | P102,500 | 25% | P800,000 |

| P2,000,000 | P8,000,000 | P402,500 | 30% | P2,000,000 |

| P8,000,000 | – | P2,202,500 | 35% | P8,000,000 |

The income tax due computation is as follows:

a = Basic Amount of Annual Income = Zero (0) b = Additional Rate = 15% c = Of the Excess over P250,000 = P50,000 INCOME TAX DUE = a + (b x c) INCOME TAX DUE = 0 + (15% * P50,000) = P7,500

Wait, what about personal and additional exemptions since Employee Z is married and has dependents? Should these exemptions be deducted from the employee’s taxable income? No, as there are no more personal and additional exemptions under the new TRAIN law.

So to recap, Employee Z who earned P300,000 taxable income in 2023 will be paying income tax of P7,500.

You’ll notice that the tax due of P7,500 is much lower than the income tax due of P10,000 during the implementation of TRAIN in 2018 to 2022 (as shown in Sample Problem #1). This is because the TRAIN law further reduced income tax rates from 2023 onwards.

Previously, the effective income tax rate charged to a taxpayer with P300,000 taxable income was 3.33%. From 2023 onwards, the new effective income tax rate, paying P7,500 income tax on P300,000 annual income, is down to just 2.5%.

How about the employee making P1 Million a year? Let’s compute the income tax payable in the next problem.

Sample Problem #4. Employee X, from Sample Problem #2, continues to work as an accountant in a company. No salary increase was given and, in 2023, her taxable income remained at P1,000,000. How much is her income tax payable that year? How much is her effective income tax rate?

Using the new graduated income tax tables for 2023 onwards (see above), her taxable income falls under the row “Above P800,000 to P2,000,000”. Employee X’s new income tax payable can be computed as follows:

a = Basic Amount of Annual Income = P102,500 b = Additional Rate = 25% c = Of the Excess over P800,000 = P200,000 INCOME TAX DUE = a + (b x c) INCOME TAX DUE = P102,500 + (25% * P200,000) = P152,500

Therefore, Employee X will have to pay income tax in the amount of P152,500. Paying P152,500 income tax on P1 Million taxable income, this taxpayer is paying an effective income tax rate of 15.25%.

Take note that in Sample Problem #2, the same employee paid income tax amounting to P190,000 in 2022. Even with no change in the amount of taxable income (P1 million), the income tax payable of P152,500 in 2023 is lower than the P190,000 income tax paid in 2022.

Also note that in 2023, Employee X’s effective income tax rate of 15.25% is much lower than the 19% effective income tax rate during the implementation of TRAIN in 2018 to 2022 (as seen in Sample Problem #2). Such is the benefit of reduced income tax rates under the TRAIN law.

Now you know how to compute your own income tax under the new TRAIN tax tables! Good job!

You must read these other awesome articles!